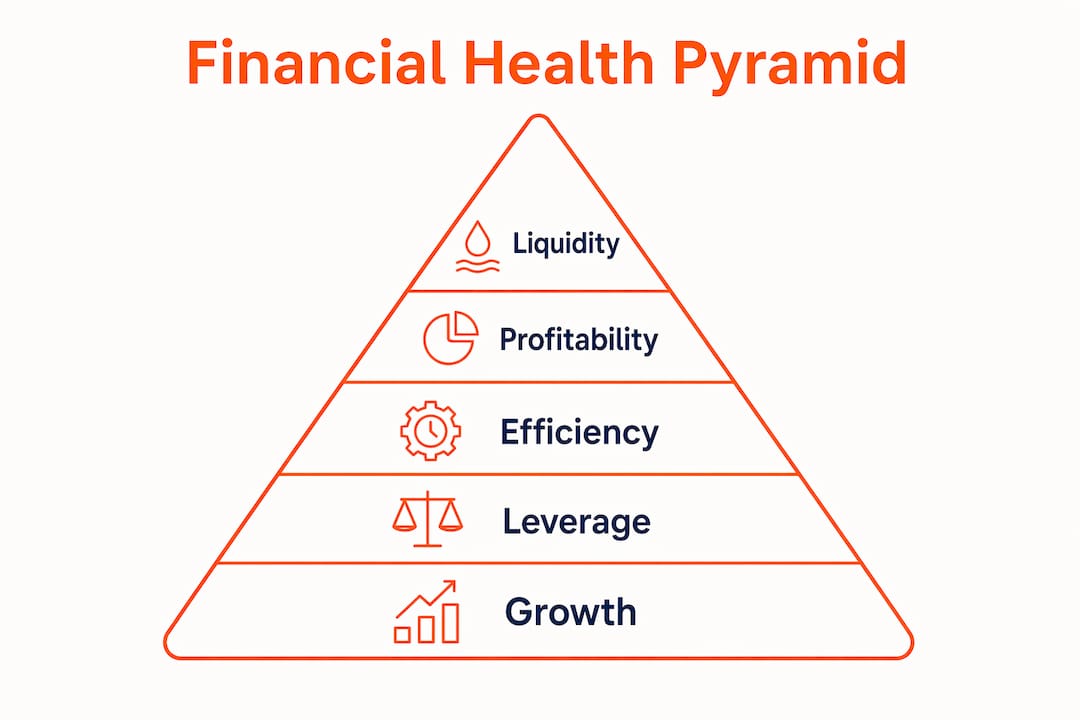

Business financial health is defined as a company's measurable ability to sustain operations, meet financial obligations, and support growth over time. Most business owners track revenue and profit, but the full picture requires evaluating six interconnected dimensions: liquidity, profitability, operating efficiency, leverage, growth trajectory, and financial controls. These dimensions, drawn from your balance sheet, income statement, and cash flow statement, tell you not just where you stand today but where you are heading. Understanding financial stability at this level is what separates reactive management from confident, informed decision-making.

What is business financial health and why does it matter?

Business financial health is the formal assessment of how well a company can survive, grow, and thrive based on specific, measurable financial criteria. The industry term for this practice is financial health assessment, and it draws on ratio analysis, trend monitoring, and benchmarking across multiple financial dimensions. A company that scores well on all six dimensions is considered financially resilient; one that underperforms across several is approaching distress.

The importance of financial health extends beyond survival. Lenders, investors, and suppliers use these same metrics to decide whether to extend credit, invest capital, or offer favorable terms. A business with strong financial health commands better loan rates, attracts talent, and weathers economic downturns with far less disruption than one that only monitors its bank balance.

The SBA recommends using the balance sheet as a snapshot to track capital, monitor assets and liabilities, and support cash flow projection. This is not a one-time exercise. Financial health is a continuous state, not a moment in time, and the companies that treat it that way consistently outperform those that only check their numbers at tax time.

What are the key financial metrics and dimensions that indicate business financial health?

A practical six-dimension framework covers every angle of financial health assessment. Each dimension uses specific ratios and metrics to produce a clear signal.

Liquidity and cash position

Liquidity measures whether you can pay short-term obligations without selling long-term assets. The current ratio (current assets divided by current liabilities) and the quick ratio (which excludes inventory) are the two primary tools. Cash runway is equally critical. It measures how many months your company can operate before depleting cash reserves at the current burn rate. Cash runway benchmarks classify under 6 months as critical, 6 to 12 months as concerning, 12 to 18 as acceptable, and over 24 months as strong health.

Profitability and operating efficiency

Profitability metrics include gross margin, net margin, and EBITDA margin. These tell you how much of each revenue dollar you actually keep after costs. Operating efficiency metrics such as days sales outstanding (DSO), inventory turnover, and the cash conversion cycle reveal how quickly your business converts activity into cash. A company can be profitable on paper while still running out of cash if its DSO is too high or its inventory sits unsold for months.

Leverage, growth, and financial controls

The debt-to-equity ratio and solvency ratios measure how much of your business is financed by debt versus owner equity. High leverage amplifies both gains and losses, so tracking this metric alongside cash flow is non-negotiable. Growth trajectory indicators show whether revenue, margins, and customer acquisition are moving in the right direction at a sustainable pace. Financial controls and reporting quality round out the framework, covering whether your data is accurate, timely, and organized enough to support real decisions.

| Dimension | Key Metric | What It Signals |

|---|---|---|

| Liquidity | Current ratio, cash runway | Ability to meet short-term obligations |

| Profitability | Gross margin, EBITDA margin | Revenue retained after costs |

| Operating efficiency | DSO, inventory turnover | Speed of converting activity to cash |

| Leverage | Debt-to-equity ratio | Reliance on debt financing |

| Growth trajectory | Revenue growth rate | Sustainability of expansion |

| Financial controls | Reporting accuracy and timeliness | Reliability of financial data |

Pro Tip: Track your cash runway every month, not just quarterly. A business with 18 months of runway in January can drop to 9 months by June if burn rate increases and no one catches it early.

How can you interpret and analyze financial health indicators effectively?

Reading a ratio is easy. Knowing what it means for your specific business takes more skill. The key distinction is between leading and lagging indicators. Lagging indicators like net profit and revenue confirm what already happened. Leading indicators like DSO, pipeline conversion rates, and order backlog signal what is about to happen. Businesses that focus only on lagging indicators are always reacting. Those that track leading indicators can intervene before problems compound.

Four analysis techniques give you the most complete picture:

- Trend analysis: Compare the same metric across multiple periods (monthly, quarterly, annually) to spot directional movement. A declining gross margin over six quarters is a warning sign even if the absolute number still looks acceptable.

- Correlation analysis: Identify which operational drivers move your financial outcomes. If your DSO rises every time you onboard a new sales rep, that correlation points to a process gap in collections training.

- Variation analysis: Measure actual results against budget or forecast. Large, unexplained variances signal either poor planning or operational problems worth investigating.

- Event analysis: Isolate the financial impact of specific events such as a product launch, a price increase, or a major customer loss to understand cause-and-effect relationships in your numbers.

Benchmarking adds external context. Comparing your gross margin to industry averages from sources like the U.S. Census Bureau's Annual Survey of Manufactures or sector-specific databases tells you whether your performance reflects a business problem or an industry-wide condition. Internal benchmarking, comparing your current performance to your own historical best, is equally valuable for setting realistic improvement targets.

No single metric tells the full story. Positive operating cash flow combined with a deteriorating current ratio and rising DSO paints a very different picture than each metric viewed in isolation.

Pro Tip: Use rolling 12-month periods instead of calendar-year snapshots. Rolling periods smooth out seasonal distortions and give you a cleaner read on true trend direction.

What practical steps can you take to assess and improve financial health?

A structured business financial assessment does not require a finance department. It requires discipline, the right tools, and a consistent schedule. Here is a numbered process that works for most small and mid-sized businesses:

- Collect your three core statements. Pull your balance sheet, income statement, and cash flow statement for the current period and the prior three periods. Computing ratios across liquidity, solvency, profitability, and operating efficiency starts here.

- Calculate your six-dimension metrics. Use the framework above. Flag any metric that falls outside acceptable benchmarks for your industry.

- Identify your weakest dimension. Prioritize it. If liquidity is the problem, focus on accelerating receivables and renegotiating payment terms before addressing anything else.

- Build a 13-week cash flow forecast. This short-term rolling forecast is the single most practical tool for managing liquidity in real time.

- Run a scenario stress test. Model what happens to your cash position if your largest customer delays payment by 60 days, or if a key supplier raises prices by 15%. Scenario analysis informs financing and working capital decisions before a crisis forces your hand.

- Set a monitoring cadence. Quarterly reviews work for stable businesses. Monthly reviews are appropriate for businesses with volatile revenue or high fixed costs.

- Engage professional support when needed. A CPA or fractional CFO brings benchmarking data, tax optimization, and strategic perspective that accounting software alone cannot provide. Tools like QuickBooks, Xero, and Fathom HQ automate ratio tracking and flag anomalies, but human interpretation remains the deciding factor.

Improvement tactics follow naturally from your weakest dimension. To improve liquidity, tighten your collections process and negotiate extended payment terms with suppliers. To improve profitability, audit your cost structure and identify products or services with below-average margins. To reduce leverage, prioritize debt repayment from free cash flow before pursuing growth spending.

Pro Tip: Integrate financial and non-financial data in your reviews. Customer churn rates, employee turnover, and supplier lead times are non-financial signals that often predict financial deterioration weeks before it shows up in your ratios.

What common challenges can affect business financial health?

Several patterns consistently undermine the financial health of a business, and most of them are invisible until they reach a critical stage.

- Cash flow gaps despite profitability. A business can show net profit on its income statement while simultaneously running out of cash. This happens when revenue is recognized before cash is collected, or when growth requires heavy upfront investment in inventory and payroll.

- Overleveraging. Taking on debt to fund growth is rational up to a point. When debt service consumes a large share of operating cash flow, any revenue shortfall becomes an immediate solvency threat.

- Growth masking deterioration. Rapid growth can hide declining unit economics and unsustainable burn rates. A company growing revenue at 40% annually while its gross margin compresses from 60% to 42% is not winning. It is accelerating toward a cliff.

- Insufficient cash runway. A runway of under 6 months is classified as critical. Many businesses only discover this when payroll is at risk, by which point options are severely limited.

- Weak financial controls. Inaccurate or delayed financial reporting means decisions are made on bad data. This is not just an accounting problem. It is a strategic risk.

Early warning signs include rising DSO, declining quick ratio, increasing reliance on short-term credit lines to fund operations, and a widening gap between net income and operating cash flow. Catching these signals early is the entire point of regular financial health monitoring.

Key takeaways

Strong business financial health requires tracking six dimensions simultaneously, not just profit and revenue, and acting on leading indicators before lagging ones confirm a problem.

| Point | Details |

|---|---|

| Six-dimension framework | Assess liquidity, profitability, efficiency, leverage, growth, and controls together for a complete picture. |

| Cash runway is critical | Under 6 months of runway signals a financial emergency; monitor it monthly, not quarterly. |

| Lead with leading indicators | DSO, pipeline data, and order backlog predict problems before net profit confirms them. |

| Stress test regularly | Model delayed payments and cost shocks to make financing decisions before a crisis forces them. |

| Combine data types | Integrate financial ratios with non-financial signals like churn and supplier lead times for better decisions. |

What I have learned about financial health after years in lending

After working with hundreds of businesses across loan applications and financial reviews at Ryves-finance, one pattern stands out above all others: the businesses that struggle most are not the ones with the worst numbers. They are the ones who stopped looking at their numbers regularly.

A business owner who reviews their current ratio monthly and sees it drop from 2.1 to 1.4 over six months has time to act. They can tighten collections, renegotiate a supplier contract, or draw on a credit facility at favorable terms. The owner who only looks at the numbers when something feels wrong discovers the same drop at 0.9, when options are expensive and time is short.

The other thing I have seen consistently is the trap of growth optimism. Revenue going up feels like success, and it often is. But growth trajectory must be assessed alongside profitability and cash flow, not instead of them. I have reviewed loan applications from companies with impressive top-line growth and a cash runway of four months. That is not a healthy business. That is a fast-moving one heading toward a wall.

My honest advice: treat your financial health check the same way you treat a vehicle inspection. You do not wait for the engine warning light. You schedule it, you run through the checklist, and you fix small problems before they become expensive ones. The businesses that do this consistently are the ones that come to us from a position of strength, not desperation.

— Ryves

How Ryves-finance supports your business financial health

At Ryves-finance, we work with business owners who want to make smarter financial decisions, not just access capital. Whether you are looking to improve your cash position, manage existing debt more effectively, or fund a growth phase with the right structure, our team provides integrated financial advice tailored to your specific situation.

We specialize in business lending solutions that prioritize the best repayment terms and the least onerous credit agreements for your business. Our approach starts with understanding your financial health across the dimensions that matter most to lenders and to your long-term stability. If you are ready to take a clear-eyed look at your company's finances and access support that fits your goals, visit Ryves-finance today to get started.

FAQ

What is business financial health in simple terms?

Business financial health is a company's ability to pay its bills, sustain operations, and grow over time, measured through ratios and metrics across liquidity, profitability, efficiency, leverage, and growth.

What are the most important indicators of financial health?

Positive and stable operating cash flow is among the strongest single indicators, but a complete picture requires evaluating the current ratio, gross margin, debt-to-equity ratio, and cash runway together rather than in isolation.

How often should a business assess its financial health?

Stable businesses should conduct a formal financial health assessment quarterly. Businesses with volatile revenue, high fixed costs, or rapid growth should review key metrics monthly to catch deterioration early.

What is cash runway and why does it matter?

Cash runway measures how many months a company can operate before depleting its cash reserves at the current burn rate. Under 6 months is classified as critical, making it one of the most urgent metrics to monitor.

Can a profitable business still have poor financial health?

Yes. A business can report net profit while running out of cash if receivables are slow, debt service is high, or growth requires heavy upfront spending. This is why operating cash flow must be tracked alongside profitability metrics.