A personal loan is an unsecured, fixed-term credit product that teachers can use for classroom supplies, debt consolidation, moving costs, or income smoothing during summer pay gaps. This teacher personal loan application guide walks you through every stage of the process, from checking your eligibility to managing your repayments after funding. Teachers are a distinct borrower group, and lenders like Teachers Federal Credit Union and Educational Employees Credit Union offer underwriting terms that general banks rarely match. The NEA reports that teachers spend hundreds of dollars of their own money annually on professional needs, making personal loans for teachers a practical and often necessary financial tool. Follow this guide and you will apply with confidence, compare offers intelligently, and protect your credit score throughout.

What are the eligibility requirements for teacher personal loan applications?

Lenders evaluate teachers using the same core criteria they apply to any borrower, but teacher-focused institutions add flexibility that makes approval more realistic for educators on fixed salary schedules. Understanding these requirements before you apply is the single most effective way to avoid delays.

Standard eligibility criteria

Common eligibility criteria for teacher personal loans include stable employment, a minimum income threshold, a satisfactory credit score, and a clean repayment history. Traditional banks typically require a credit score of 750 or above, while teacher-focused credit unions often accept scores in the 680 to 720 range because they understand the structured nature of educator income. Your employment status matters too. Full-time teachers at accredited institutions are viewed more favorably than part-time or substitute teachers, though some credit unions accommodate non-traditional contracts.

Documentation you need to prepare

Gathering your documents before you start any application saves significant time and prevents the most common reason for application delays: missing paperwork. Here is what most lenders require:

| Document | Traditional Banks | Teacher-Focused Credit Unions |

|---|---|---|

| Government-issued photo ID | Required | Required |

| Recent pay stubs (2 to 3 months) | Required | Required |

| Employment verification letter | Required | Sometimes waived with teaching credentials |

| Teaching license or credentials | Rarely requested | Frequently requested and used favorably |

| Bank statements (2 to 3 months) | Required | Required |

| Tax returns (1 to 2 years) | Often required | Sometimes optional for salaried staff |

| Proof of address | Required | Required |

Teacher-focused lenders treat your teaching license as a signal of professional stability, which can work in your favor during underwriting. Traditional banks rarely factor in your credential status and rely almost entirely on credit score and income figures.

Pro Tip: Pull your free credit report from AnnualCreditReport.com and request an employment verification letter from your school district's HR department before you submit a single application. Resolving any errors on your credit report before applying can raise your score by 20 to 50 points, which directly affects the APR you are offered.

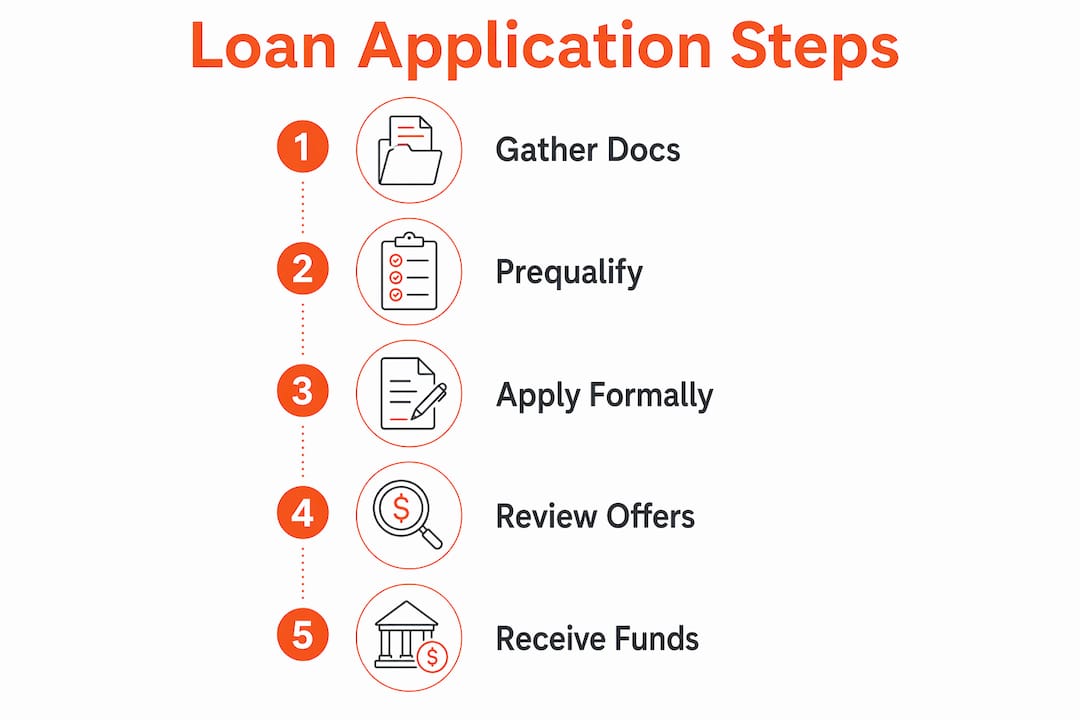

How to apply for a personal loan as a teacher, step by step

The personal loan application process follows a clear sequence: check your credit score, determine your loan amount, prequalify, compare offers, apply formally, and review the final offer before accepting. Each step builds on the last, and skipping any one of them increases the risk of a poor outcome.

-

Check your credit score. Use a free service like Experian, Credit Karma, or your bank's built-in credit monitoring tool. Know your number before any lender does. A score below 670 signals that you may need to spend 60 to 90 days improving it before applying.

-

Calculate the loan amount you actually need. Write down the specific expense or goal, then add a 10 percent buffer for unexpected costs. Borrowing more than you need increases your total interest paid and your monthly payment burden.

-

Estimate your monthly payment. Use a free online loan calculator to model different loan amounts and term lengths. A $10,000 loan at 12% APR costs $1,950 in interest over three years but $3,350 over five years. Choosing the shorter term saves real money if your monthly budget allows it.

-

Prequalify with multiple lenders. This is the most underused step in the teacher loan application process. Prequalification uses a soft credit inquiry that does not affect your credit score, so you can check estimated rates from three to five lenders without any penalty.

-

Compare all offers side by side. Look at APR, loan term, origination fees, prepayment penalties, and funding speed. Do not make a decision based on the monthly payment alone.

-

Submit your formal application. Once you select the best offer, complete the full application. This triggers a hard credit inquiry, which typically reduces your score by five to ten points temporarily.

-

Review the loan agreement carefully. Read every line before signing. Confirm the APR, repayment schedule, any fees, and the total cost of the loan. If anything differs from your prequalification estimate, ask the lender to explain the discrepancy in writing.

Most lenders fund approved personal loans within one to three business days. Teacher-focused credit unions may take slightly longer due to membership verification, but their rates often justify the wait.

Pro Tip: Prequalify with at least three lenders before submitting a single formal application. This protects your credit score and gives you real rate data to use as negotiating leverage.

How to compare personal loan offers tailored for teachers

Comparing loan offers is where most borrowers make costly mistakes. The monthly payment figure is the least useful number on any loan offer. Focus on APR and total repayment cost instead.

APR matters more than the interest rate alone because it includes origination fees and other lender costs. A loan advertised at 12% interest with a 5% origination fee is more expensive than a loan at 14% interest with no fees, depending on the loan term. Always ask for the APR and the total repayment amount before comparing.

Key factors to evaluate in every loan offer

- APR: The single most reliable number for comparing total loan cost across lenders.

- Loan term: Shorter terms mean higher monthly payments but significantly less total interest paid.

- Origination fees: Some lenders charge 1% to 8% of the loan amount upfront. This reduces the cash you actually receive.

- Prepayment penalties: Avoid any loan that charges a fee for paying off early. Teachers who receive summer bonuses or tax refunds should have the freedom to pay down principal without penalty.

- Funding speed: If you need cash for an urgent classroom expense or moving cost, a lender that funds in 24 hours is worth a slightly higher rate than one that takes two weeks.

- Membership requirements: Teacher-focused credit unions like Teachers Federal Credit Union require membership, but the process is typically straightforward for licensed educators.

Teacher-focused credit unions frequently offer lower APRs than general market lenders, with rates starting around 9.99% APR at institutions like Teachers Federal Credit Union and Educational Employees Credit Union. That difference of even two to three percentage points on a $15,000 loan translates to hundreds of dollars saved over a three-year term.

Online marketplaces that use soft credit pulls, such as loan comparison platforms, let you see multiple offers in one place without triggering hard inquiries. This is the fastest way to build a comparison set before committing to any single lender.

What mistakes should teachers avoid when applying for personal loans?

The education loan application process is straightforward when you prepare properly, but several common errors can delay approval, reduce your loan amount, or increase your cost of borrowing.

- Applying to multiple lenders simultaneously without prequalifying first. Hard inquiries from multiple applications can lower your credit score and signal financial distress to lenders. Always prequalify first.

- Submitting incomplete documentation. Missing a single document, such as an employment verification letter or a recent bank statement, can pause your application for days.

- Ignoring fees and penalties in the loan agreement. Origination fees and prepayment penalties are buried in the fine print but can add hundreds of dollars to your total cost.

- Borrowing more than your repayment plan supports. Calculate your monthly payment against your take-home pay before accepting any offer. A general rule is that total debt payments should not exceed 36% of your gross monthly income.

- Confusing personal loans with teacher loan forgiveness programs. Personal loans and Public Service Loan Forgiveness (PSLF) are entirely separate products. PSLF applies to federal student loans, not personal loans.

If your application is denied, ask the lender for the specific reason in writing. Common causes include a credit score below the lender's threshold, a high debt-to-income ratio, or insufficient income documentation. Address the specific issue before reapplying, ideally after 60 to 90 days.

Pro Tip: Most lenders offer an online application portal where you can track your application status in real time. Log in every 24 to 48 hours after submitting to catch any requests for additional documentation before they cause delays.

How can teachers manage personal loans after approval?

Approval is not the finish line. How you manage your loan after funding determines whether it helps or hurts your financial health over the long term.

- Set up automatic payments immediately. Most lenders offer a 0.25% APR discount for autopay enrollment. More importantly, automatic payments eliminate the risk of a missed payment, which is the fastest way to damage a credit score you worked hard to build.

- Track your payoff date and remaining balance monthly. Use a simple spreadsheet or a free app like Mint or YNAB to monitor your loan alongside your other financial obligations.

- Ask your credit union about skip-a-payment options. Some teacher-focused credit unions offer a skip-a-payment feature during summer months when educators on 10-month contracts experience income gaps. This option typically costs a small fee but prevents missed payments from appearing on your credit report.

- Use the loan to consolidate higher-interest debt if that was your goal. Once funded, pay off the targeted debts immediately. Do not let the consolidation loan sit in your checking account while high-interest balances continue to accrue.

- Monitor your credit score monthly. Experian, TransUnion, and Equifax all offer free monitoring tools. A personal loan, when managed well, improves your credit mix and builds a positive payment history, both of which raise your score over time.

Key takeaways

Teachers who prepare their documentation, prequalify with multiple lenders, and focus on APR rather than monthly payment will secure the best personal loan terms available to educators.

| Point | Details |

|---|---|

| Prequalify before applying | Use soft credit pulls with multiple lenders to compare rates without harming your credit score. |

| APR beats interest rate | Always compare loans by APR, which includes fees, not just the advertised interest rate. |

| Teacher credit unions offer better terms | Institutions like Teachers Federal Credit Union start rates around 9.99% APR, below most general lenders. |

| Documentation preparation matters | Gather pay stubs, teaching credentials, and employment verification before starting any application. |

| Post-approval management builds credit | Autopay enrollment and monthly balance tracking protect your credit score and reduce total loan cost. |

What I have learned from working with educators on personal loans

After working with teachers across different income levels and credit profiles, one pattern stands out clearly. The educators who get the best loan terms are not always the ones with the highest credit scores. They are the ones who arrive prepared. They know their credit score, they have their documents ready, and they have already prequalified with two or three lenders before sitting down to make a final decision.

The biggest mistake I see repeatedly is treating a personal loan application the same way you would treat a quick online purchase. Teachers sometimes apply to the first lender they find, accept the first offer they receive, and only later realize they paid a 6% origination fee that a credit union would have waived entirely. That is not a small oversight. On a $12,000 loan, a 6% origination fee is $720 out of your pocket before you receive a single dollar.

My honest advice: join a teacher-focused credit union before you need a loan. Membership is usually free or low cost, and having an established relationship with an institution that understands educator income cycles gives you a real advantage when you apply. Teachers Federal Credit Union and Educational Employees Credit Union both have straightforward membership processes for licensed educators.

Personal loans are not inherently risky. They become risky when borrowers skip the comparison step or borrow without a clear repayment plan. Used correctly, a personal loan can consolidate expensive credit card debt, cover a classroom renovation, or smooth out a summer income gap without derailing your financial goals.

— Ryves

How Ryves-finance supports teachers applying for personal loans

At Ryves-finance, we built our personal loan products around one goal: giving borrowers the best price, the most manageable repayment terms, and the least burdensome credit agreement possible.

Teachers who apply through Ryves-finance benefit from a straightforward application process, transparent fee structures, and a team that takes the time to match you with a loan that fits your actual financial situation. We do not believe in one-size-fits-all lending. Whether you need funds for classroom expenses, debt consolidation, or a major life event, we work with you to find terms that make sense. Visit Ryves-finance today to start your personal loan application or speak with one of our advisors about your options.

FAQ

What credit score do teachers need for a personal loan?

Most traditional banks require a credit score of 750 or above, while teacher-focused credit unions often approve applicants with scores in the 680 to 720 range. Improving your score before applying directly lowers the APR you are offered.

Does prequalification affect my credit score?

Prequalification uses a soft credit inquiry and does not affect your credit score. Only the formal application triggers a hard inquiry, which may reduce your score by five to ten points temporarily.

What can teachers use a personal loan for?

Teachers commonly use personal loans for classroom supplies, income smoothing during summer pay gaps, moving costs, debt consolidation, and large personal expenses. The loan funds are unrestricted once deposited into your account.

How long does the teacher loan application process take?

Most lenders approve and fund personal loans within one to three business days after a completed application. Teacher-focused credit unions may take slightly longer due to membership verification steps.

Is a personal loan the same as teacher loan forgiveness?

No. Personal loans are separate credit products with fixed repayment terms and interest charges. Public Service Loan Forgiveness (PSLF) applies exclusively to federal student loans and has no connection to personal loan products.